BFC Bulletins Monthly News Digest

BFC Bulletins Monthly News Digest

Tags Blockchain Compliance

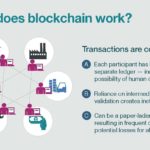

Blockchain technology has been a polarizing technology, but many are now coming to understand how it can be used to improve the know-your-customer (KYC) and anti-money laundering (AML) efforts of financial institutions. Specifically, blockchain technology offers the potential to solve existing inefficiencies, particularly those related to data asymmetries between financial institutions and regulators, duplicated compliance efforts between and within financial institutions and an excess amount of resources spent on document validation (as opposed to risk assessment). Blockchain technology accomplishes this via a centralized platform that the regulator and approved financial institutions have access to. This allows for the efforts of one financial institution to benefit all others, with consumer-specific data continually updated and shared among all platform users. This ensures that data is consistent and up-to-date as well as that resources are spent toward analysis and not validation.

While there are still some issues to be overcome for such a platform to become a reality (e.g. data-privacy concerns, ensuring the buy-in of financial institutions), the interconnectedness of the modern world means that information sharing will become more and more the norm. Moreover, consumers will expect financial institutions to access and use this information quickly and efficiently in order to provide them with appropriate services, all while ensuring information is safeguarded. Blockchain technology is likely an inevitability for the future of compliance.